mutual fund

Currently we do not provide any mutual fund service, we will launch it in future.

what is mutual fund ?

A mutual fund is a type of investment vehicle that pools money from many investors to invest in securities such as stocks, bonds, money market instruments, and other assets. These funds are managed by professional portfolio managers who make investment decisions on behalf of the investors.

Are mutual funds safe?

Investing in a mutual fund is not safe as its performance is linked to the market. Mutual funds are also affected by the economy as a whole. The price of each unit may fluctuate daily. When the markets tumble, so do your mutual funds.

How Do Mutual Funds Work?

To understand how mutual funds work, let us first understand the concept of NAV (Net Asset Value). NAV per unit is the price at which investors can buy or redeem their mutual fund investments. Investors in mutual funds are allotted units proportional to their investments and this is calculated on the basis of the NAV. For example, if you invest Rs 500 in a mutual fund with an NAV of Rs 10, you will get (500/10), 50 units of the mutual fund.

Now, the NAV of the mutual fund changes every day on the basis of the performance of the assets in the mutual fund is invested in. If a mutual fund invests in a particular stock whose price goes up tomorrow, the same will reflect in the NAV of the mutual fund and vice versa. So, in the above example, if the NAV of the mutual fund goes up to Rs 20, then your 50 units that amounted to Rs 500 earlier will now amount to Rs 1000 (500 units x Rs 20). Hence, the mutual fund’s performance is driven by its underlying assets, which generate its returns to investors.

So, if you redeem your mutual fund units, you shall receive Rs 1000 against the Rs 500 you originally paid. This gain of Rs 500 is known as a capital gain. The market value of the mutual fund portfolio is not fixed but varies every day; consequently, NAV also tends to change daily, based on the valuation of the fund portfolio. Hence, this gain of Rs 500 can be a loss also, depending on how the NAV moves and the underlying assets perform. Since mutual fund investments are market-linked, the returns are not guaranteed and are also, dynamic in nature.

Mutual fund returns (capital gains) are subject to tax, known as capital gains tax. Capital gains tax will impact when you choose to redeem your investment; like in the example above you will be liable to pay a tax on the Rs 500 you have earned. Bear in mind two things though:

- The capital gains tax is applicable only if you redeem the investment and not if you stay invested.

- The extent of capital gains tax will depend on the types of mutual funds and your investment holding.

Mutual funds are subject to short-term capital gains tax (STCG) and long-term capital gains tax (LTCG). The periods of short-term and long-term capital gains tax are defined differently for mutual funds.

Types of Mutual Funds

There are multiple ways in which mutual funds can be categorized, for example, the way they are structured, the kind of securities they hold, their investment strategies, etc. The Securities and Exchange Board of India (SEBI) has classified mutual funds based on where they invest, some of which we have listed below.

Based on the structure:

- Open-ended funds are mutual funds that allow you to invest and redeem investments at any time, i.e. they are perpetual in nature. They are liquid in nature and don’t come with a specific investment period.

- Close-ended schemes have a fixed maturity date. You can only invest at the time of the new fund offer and redemption can only be done on maturity. You cannot purchase the units of a close-ended mutual fund whenever you please.

Based on asset classes:

- Equity Mutual Funds invest at least 65% of their assets in stocks of companies listed on the stock exchange. They are more suitable as long-term investments (> 5 years) as stocks can be volatile in the short term. They have the potential to offer higher returns but also come with high risk.

- Debt Mutual Funds primarily invest in fixed-income instruments like Government securities, corporate bonds, and other debt instruments. They are not affected by stock market volatility and hence, can offer more stable returns compared to equity mutual funds. The types of debt mutual funds are differentiated on the basis of the maturity period of the securities they hold.

- Hybrid Mutual Funds invest in both equity and debt in varying proportions depending on the investment objective of the fund. Thus, hybrid funds give you diversified exposure to various asset classes. Hybrid funds are categorized on the basis of their allocation to equity and debt.

Ways/modes of Mutual Fund Investment

An investor can invest in mutual funds in the following ways:

- Lumpsum: When you want to invest a significant amount in a mutual fund in one go. For example, if you had a sum of Rs 1 lakh to invest then you could go in for lumpsum investment and invest the entire amount of Rs 1.0 lakh at one go in a mutual fund of your choice. The units allotted to you will depend on the NAV of that fund on that particular day. If the NAV is Rs 1000, you will end up getting 100 units of the mutual fund.

- SIP: You also have the option to invest small amounts periodically. In the above example, say, you don’t have Rs 1 Lakh but can commit to an investment of Rs 10,000 per month for 10 months, and you can align your investments with your cash flows. This way of investing is known as a Systematic Investment Plan (SIP). SIP encourages regular investment of fixed amounts bi-monthly, monthly, quarterly and so on, depending on your need and the options available with the mutual fund.

This method of investing inculcates a discipline of investment and also eliminates any need to look for the right time to invest. Many investors try to time the market which generally requires considerable time and expertise. What a SIP does instead is to average out your costs and the investor doesn’t need to time the market. When the NAV is low, it gets you higher units and vice versa. SIPs, when done regularly over the long term, can help you build a more considerable mutual fund investment corpus.

The minimum amount for a lump sum and SIP investments are defined by mutual fund companies and can vary but can start at as low as Rs 100.

How To Invest in Mutual Funds?

Broadly there are three ways to invest in mutual fund schemes:

- Through a Mutual Fund company’s website

- Through a Mutual Fund distributor

- Through the ET Money

If you want to invest through a mutual fund company’s website, you will need to sign up and create an account. Then follow the ensuing steps. However, there’s a major challenge with this route.

Most likely, you will find schemes of different fund houses attractive. To invest in them, you have to sign up with each fund house. And that could be a huge hassle. It would also be challenging to track your investments and analyze them.

The second option is to invest via a mutual fund distributor. But this isn’t a cost-effective way. You will pay a higher expense ratio, and, as a result, your returns will be lower.

A much simpler, more efficient, and effective way of investing in mutual fund schemes is the third option – through the ET Money platform.

All you need to do is sign up once and start investing in schemes from different AMCs. You can choose from various schemes of various Mutual Fund companies. More importantly, you will be able to do it at a lower expense ratio because ET Money is a direct investment platform.

You can also track your existing portfolio on ET Money. You can view all your old and new investments in one place, making it much simpler to track them and make better-informed decisions.

In addition to the above, the ET Money investment platform also offers valuable details like the fund’s past performance, returns consistency, downside protection, fund history, expense ratio, exit load, and other essential information.

What are the documents required to invest in mutual funds?

The documents for KYC (Know Your Client) include proof of address and proof of identity. Here is a list of officially valid documents (OVD) admissible.

PROOF OF IDENTITY:

- PAN Card (Mandatory)

- Voter ID Card

- Driving License

- Passport

- Aadhaar Card

- Any other valid identity card issued by the Central or State Government

PROOF OF ADDRESS

- Voter ID Card

- Driving License

- Passport

- Ration Card

- Aadhaar Card

- Bank account statement or bank passbook

- Utility bills like electricity or gas bills

While these are some of the standard documents, submitting all of these documents is a tedious process and can procrastinate your plan of investment. This is where ET Money offers you a paperless and fast solution.

You can submit your KYC in under two minutes by uploading photos of your identity and address proof. This includes PAN and any one of your Aadhaar, Voter ID, Driving License, and passport along with your signature, a selfie, and a live video authenticating your identity. ET Money’s quick KYC application makes investing easy and hassle-free.

It takes about 3–5 working days to get your KYC verified as the verification is done by government-certified agencies.

Features & Benefits of Mutual Funds

Now that we know what mutual funds are and how they work along with their types, let us look at the advantages of investing in mutual funds.

- Diversification: The saying ‘do not put all your eggs in one basket’ perfectly fits mutual funds as spreading investment across multiple securities and asset categories lowers risk. For example, compared to direct equity investing, where your funds are deployed in individual company stocks, equity mutual funds invest in a basket of stocks across sectors, thereby reducing risk.

- Professional management: Mutual funds are managed by full-time, professional fund managers who have the expertise, experience, and resources to actively buy, sell, and manage investments. A fund manager continuously monitors investments and rebalances the portfolio accordingly to meet the scheme’s objectives.

- Transparency: Every mutual fund has a Scheme Information Document readily available on the fund house’s website that can give you all the details about its holdings, fund manager, etc. In addition, the portfolio investment value (NAV) is published daily on the AMC site, and AMFI site for investors to track the portfolio of the mutual fund.

- Liquidity: You can redeem your investments on any business/working day at the NAV of the day of your redemption. So, depending on the type of mutual fund you have invested in, you will receive your invested funds in your bank account in 1-3 days.

However, close-ended funds allow redemption only at the time of the maturity of the mutual fund. Similarly, ELSS mutual funds have a lock-in period of three years. - Tax Savings: Investment of up to Rs. 1,50,000 in ELSS mutual funds qualifies for tax benefit under section 80C of the Income Tax Act, 1961. Mutual fund investments, when held for a longer term, are tax-efficient.

- Choice: There are many options to invest in mutual funds to meet your different needs. To name a few- Liquid funds, are for investors looking to benefit from the safety of debt and low-interest rate risk, flexi-cap funds if you are looking for stock diversification, and solution-oriented mutual funds if you are looking to invest for a particular goal like retirement or children’s education, etc.

- Cost-effective: Mutual funds are a low-cost investment vehicle. The pooled investments from several investors in a mutual fund enable the fund to invest in a basket of stocks and debt securities which otherwise may be out of reach for the ordinary investor or require a higher investment amount. Thus, these pooled investments provide advantages of economies of scale. In return, lower costs to investors, such as brokerage, etc., are addressed in the minor form of fund expenses. This is why investing in direct mutual funds through ET Money makes sense because that helps you decrease the cost further.

- Returns: Mutual fund returns are not assured by mutual funds and are subject to market risks. But over the long term, equity mutual funds have the potential to deliver double-digit returns annually. Debt funds can also offer higher returns as compared to bank deposits. You can also calculate your potential returns, using a mutual fund calculator.

- Well Regulated: In India, the mutual fund industry is regulated by the capital market regulator Securities and Exchange Board of India (SEBI). Therefore, mutual funds must follow stringent rules and regulations, ensuring investor protection, risk mitigation, liquidity, and fair valuation.

Disadvantages of Mutual Funds

Now, let us have a look at the cons of investing in mutual funds.

- Exit Load: Mutual funds generally levy an exit load (fee) for redeeming investments within a specified period, for example, one year from the date of investment. This is done to refrain the investor from exiting the scheme too early, as it impacts both the fund’s performance and the investor’s goal achievement. When investing directly in stocks, say, you do not face any exit load and in comparison, this may seem like an added expense. However, this has been introduced in the investors’ interest.

- High cost: SEBI has defined the maximum limit of expense ratios that mutual fund houses can charge and they depend on the mutual fund’s size. As the size grows, the expense tends to come down. The maximum expense ratio that is chargeable for an equity-oriented mutual fund is 2.25%. And you have to bear this charge irrespective of the performance of the fund. When compared to another mode of investment, say, direct stocks, you may find the expense ratio to be higher than the brokerage you pay. But then it is being paid for the convenience and expertise, so, it is a balance that you need to achieve.

- Over-diversification: In the quest to diversify your investments, you may invest in mutual funds, which invest in a vast number of stocks, leading to over-diversification. Not all the stocks of a portfolio would deliver high returns all the time. You may end up investing in two mutual funds holding similar portfolios which may then lead to over-diversification. It is advisable to study the mutual fund portfolio before you invest.

- Risk: Investments in mutual funds are subject to market risk. The risk of losses faced by all types of securities in the financial markets cannot be reduced by diversification. Market risks may occur due to many macro and microeconomic factors. For example, equity mutual funds are subject to volatility risk owing to fluctuations in the stock market whereas debt mutual funds are subject to interest rate risk which is caused by fluctuations in the interest rates and so on.

Mutual Fund Functions

To understand mutual funds, let’s see how they function.

- New fund offer (NFO) release: An AMC can start a mutual fund scheme by launching its NFO. It creates and shares the strategy of the scheme before its launch. Investors can then decide whether and how much they should invest. NFO units are often priced at a low ticket, such as Rs 10.

- Pooling money: After the NFO, fund houses receive funds from interested investors to purchase shares in stocks, bonds, and other assets. Investors who didn’t participate in the NFO can still buy the units of the fund after it gets operational.

- Investments in securities: The scheme’s strategy determines how the fund manager will invest the funds. The fund manager does extensive research on the economy, industries, and companies before making an investment decision. He then buys the most appropriate securities that will generate optimum returns for unitholders.

- Return of funds: As mutual funds generate returns, the gains can be distributed among investors or retained in the scheme for further growth. Investors receive payouts if they choose the IDCW option (income distribution cum capital withdrawal). If they choose the growth option, the gains are retained in the scheme and allowed to grow further.

Mutual Fund Objectives

Mutual funds seek to fulfill the following objectives for their unitholders:

- Diversification: It is usually advised not to put all your eggs in one basket. Doing so can disproportionately increase your risk. Mutual funds are inherently diversified. They diversify across securities, assets, and even geographies. Hence, they help lower the risk.

- Capital protection: Some mutual funds, such as money-market funds and liquid funds, aim to protect your capital. However, while they are relatively safer, they also have lower returns.

- Capital growth: Certain mutual funds, such as equity funds, focus on growth to protect your investment against inflation. These funds invest in stocks and have higher returns but also come with higher risks.

- Saving tax: A certain class of mutual funds, called equity-linked savings schemes (ELSS) or tax-saving funds, also provide income-tax deductions up to Rs 1.5 lakh in a financial year in the old income-tax regime.

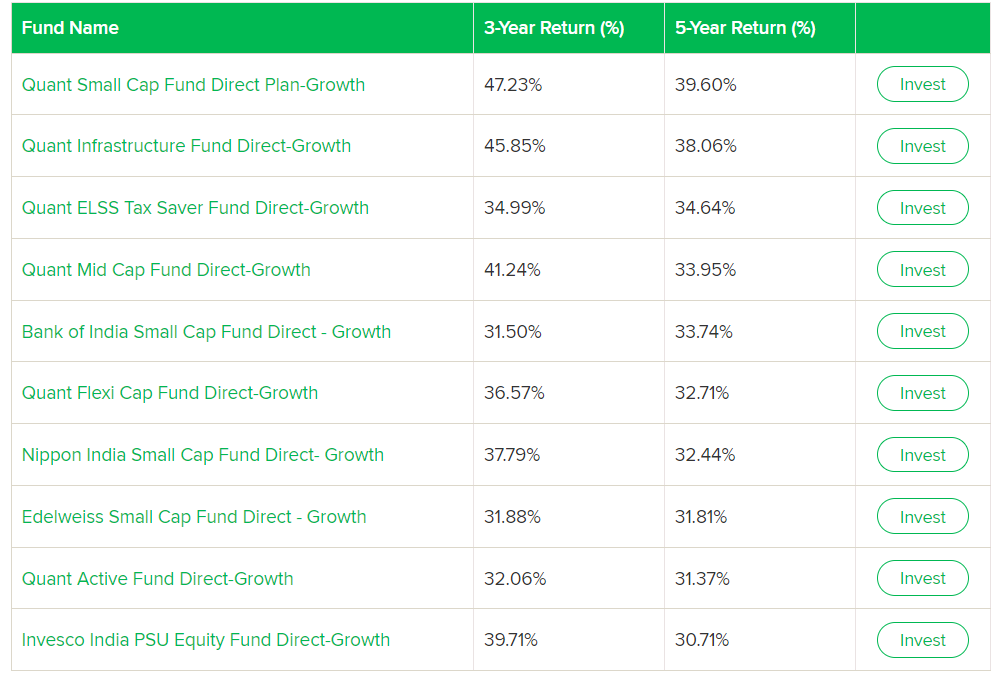

Best Mutual Fund Schemes

Here list of the best mutual funds on the basis of 5-year returns:

Terms Used in Mutual Funds

|

Terms you may encounter in Mutual Fund Investing |

Description |

|

AMC or Fund Houses |

Asset Management Company is an organization created by the sponsor of the mutual fund to help manage all activities related to the management of the mutual fund, marketing and promoting the mutual fund, and other activities from launch to collections and investments as per the fund’s investment objectives and facilitate investor transactions. |

|

NAV |

Net Asset Value -is the market value of the investment portfolio of the mutual fund divided by the total number of units of the mutual fund. NAV is the price at which mutual funds can be purchased or redeemed by the investor. |

|

SIP |

A systematic investment plan is the periodic and regular investment mode used by investors to invest in mutual funds, which helps average out the investment cost. SIP can be done monthly, or quarterly as may be desired by the investor. |

|

NFO |

New Fund Offer indicates when the mutual fund opens up for investments from investors for the first time. This period is usually fifteen days. |

|

AUM |

Assets Under Management is the total value of the portfolio of investments managed by the mutual fund |

|

CAGR |

The compound annual growth rate (CAGR) is the proportional growth rate from year to year for a mutual fund |

|

EXIT LOAD |

Exit Load is the fee charged by AMCs to investors who exit the mutual funds during the lock-in period and redeem their investments. |

|

XIRR |

XIRR stands for extended internal rate of return. It is used when investments have happened in tranches over a period of time, with withdrawals also happening in between. It is thus the aggregate returns on your investments when both inflows and outflows are involved in an irregular fashion. |

Are mutual funds taxable?

The gains from mutual funds are taxable after redemption. Tax on Short Term Capital Gains (STCG) and Long Term Capital Gains (LTCG) will apply as per the holding period and type of fund.A tax of 15% will apply if you redeem units of equity mutual funds after staying invested for less than one year. This is called a tax on Short Term Capital Gains (STCG). But, if you stay invested for more than one year, the Long Term Capital Gains (LTCG) above Rs.1 lakh will be taxed at 10%.In the case of non-equity funds, the short term capital gains, i.e. gains made on investments with an investment period of less than 36 months, is added to the income. LTCG or gains made after holding for 36 months is 20% after considering indexation.

Are mutual funds better than stocks?

Mutual funds and direct stock investments have their own set of pros and cons. You invest in different stocks at one time when you invest in equity mutual funds. In the case of direct equity investment, you have to invest in each of these stocks individually.

However, when you invest in stocks, you have complete control over your investments.

Are mutual funds and sip the same?

Systematic Investment Plan (SIP) is a systematic way to invest in mutual funds. Once you set up the SIP, the fund house will automatically debit the SIP amount from your bank account and credit your folio with mutual fund units.

Why are mutual funds subject to market risk?

Mutual funds carry risk because they invest in various financial instruments such as stocks, corporate bonds, and government securities. These instruments' prices are influenced by various circumstances, which might lead them to change and depreciate. Therefore, it is essential to ascertain the risk profile before investing in mutual funds.

As-uni tholder how much time will it take to receive dividends repurchase proceeds?

A mutual fund is required to despatch to unitholders dividend warrants within 30 days the declaration the dividend the redemption or repurchase proceeds within 10 working days fromdateredemption or repurchase request made by unit holder

In case failures to despatch redemption repurchase proceeds with instipulated time periodAsset Management Company is liable to pay interest as specified by SEBItime to time (15 at present)

What happens if I skip a payment of SIP?

Let’s accept it, we all forget things. There might be some situations when you might forget to pay your SIP amount on time. This might seem like a huge issue but it isn’t. They aren’t harsh to cancel the investment like how insurance and banks cancel the policy. But this can be easily cleared by issuing a standing instruction to automate your SIPs so you wouldn’t miss any. You can resume even after skipping the months you could not contribute. However, this will obviously affect the returns earned at the end.

Does my money get locked up?

No! Money is not locked up but it gets invested. It is always advised to keep the money invested to dodge market volatility but it doesn’t mean that there is a mystery man holding your funds refusing to return you. It is just being managed by the fund house. Depending on the nature of the fund, you can sell the units or surrender the units whenever you are in need of liquid cash. You might be charged an exit load depending on how early you withdraw and if you want to transfer these funds to another fund (within the same fund house) then that is also possible through STP.

How has this fund performed over the long run? Where can I get an independent evaluation of this fund?

Factsheets of mutual fund schemes would show you their past performance. Presently as per SEBI norms factsheets display 1 year returns for 3 consecutive periods, along with returns of the fund’s benchmark, and returns since inception of the fund. However it is important to check performance over long periods like 5 years or so, for investments in equity, bond and hybrid schemes. Independent fund research companies evaluate schemes on risk-return parameters, and in comparison with other schemes of the same type. They can supplement your decision-making. However we’d like to stress that past returns should not form the sole basis of selecting a scheme.